.jpg)

.svg)

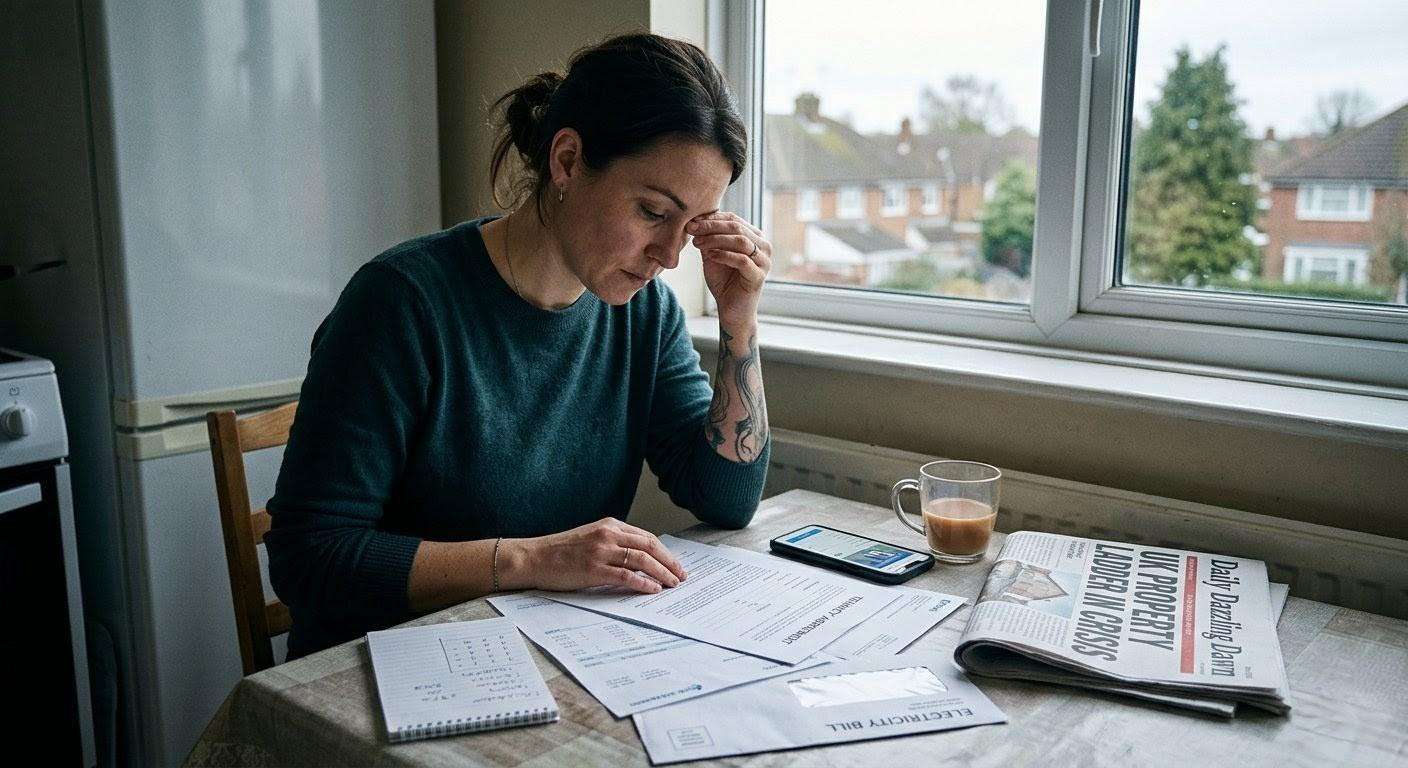

"The 'Ladder' Is Broken: Why Your First London Flat May Be a Financial Trap, Not a Stepping Stone"-For many, buying a first home in London is the ultimate dream, but for a growing number of flat owners, this step onto the property ladder is quickly turning into a financial nightmare. Starter flats, once considered a reliable springboard to a larger family home, are increasingly being dubbed "traps" as homeowners find themselves unable to 'trade up' to a house. This paralysis in the housing market is forcing many to make difficult life choices, including moving their families far from their communities, Daily Dazzling Dawn realized.

A prime example is Mr Ahmed Jamil a British Bangladeshi businessmen, who recently had to move his family to a significantly cheaper location to afford a bigger home. Chen and his partner sold their one-bedroom ground-floor garden flat in Balham, South West London, for £714,000 and bought a three-bedroom, semi-detached house in Crystal Palace, four miles further south, for £800,000. Chen, a 33-year-old estate agent, explains, "We would have loved to stay in Balham but were completely priced out." He notes that even small houses in the area now cost around £1 million, a leap far too large for many first-time flat owners.

The data confirms Chen's observation. Only 23% of people who bought their first homes in 2020 have sold them within five years, a drop from the 29% average over the past decade, according to Hamptons estate agency. Flat owners have fared the worst, with only one in 10 managing to sell, the lowest proportion since the financial crisis. A decade ago, this figure was 20%.

The core of the problem lies in the catastrophic collapse in the price growth of flats compared to houses. Since mid-2020, flat values have only risen by 15% to an average of £196,303, while detached houses have soared by 25% to an average of £437,904, according to Strutt & Parker. This contrast is compounded by the crippling costs of up-sizing. For an average first-time flat owner to move to an average detached house, the stamp duty alone is almost £12,000, which can be up to a quarter of the growth their flat has seen over five years.

Adding to the woes is the sharp increase in mortgage interest rates. Many who bought their first flats in 2020 or 2021 benefited from Covid-era rates of 2% or lower. Now, the 'effective' interest rate on newly drawn mortgages stands at 4.28%, creating a "painful jump" in monthly payments for anyone looking to remortgage or move. This is exacerbated by "front-loaded" mortgage repayments, where a large portion of early-year payments goes towards interest, slowing the accumulation of capital and limiting the deposit available for the next home. The financial stagnation is so severe that 17% of flat owners in England and Wales who sold this year actually got back less than they paid.

The ripple effects of this housing paralysis are impacting major life decisions. Housing pressures are contributing to the UK’s record-low fertility rate of 1.44, with financial uncertainty being a main reason millennials are postponing having children.

Even those who used the government's Help to Buy scheme are struggling. These flats were often sold at inflated new-build prices, and owners now face sluggish price growth, competition from newer schemes, and the repayment of the government equity loan as a share of the sale price. With cladding concerns, fire-safety issues, and rapidly rising service charges for leasehold homes, new-build flats are particularly vulnerable to depreciation.

The dream of a first home is still alive, but prospective buyers are changing their strategy, often skipping flats altogether and going straight for houses. Barclays mortgage data shows that semi-detached properties now account for 33.5% of first-time buyer purchases, up 1.7% year-on-year, while flats declined in popularity by 2.7%, making up only 19.6% of sales. Unless there is a significant shift in the market dynamics between flats and houses, that coveted first step onto the property ladder may continue to be a trap for many.